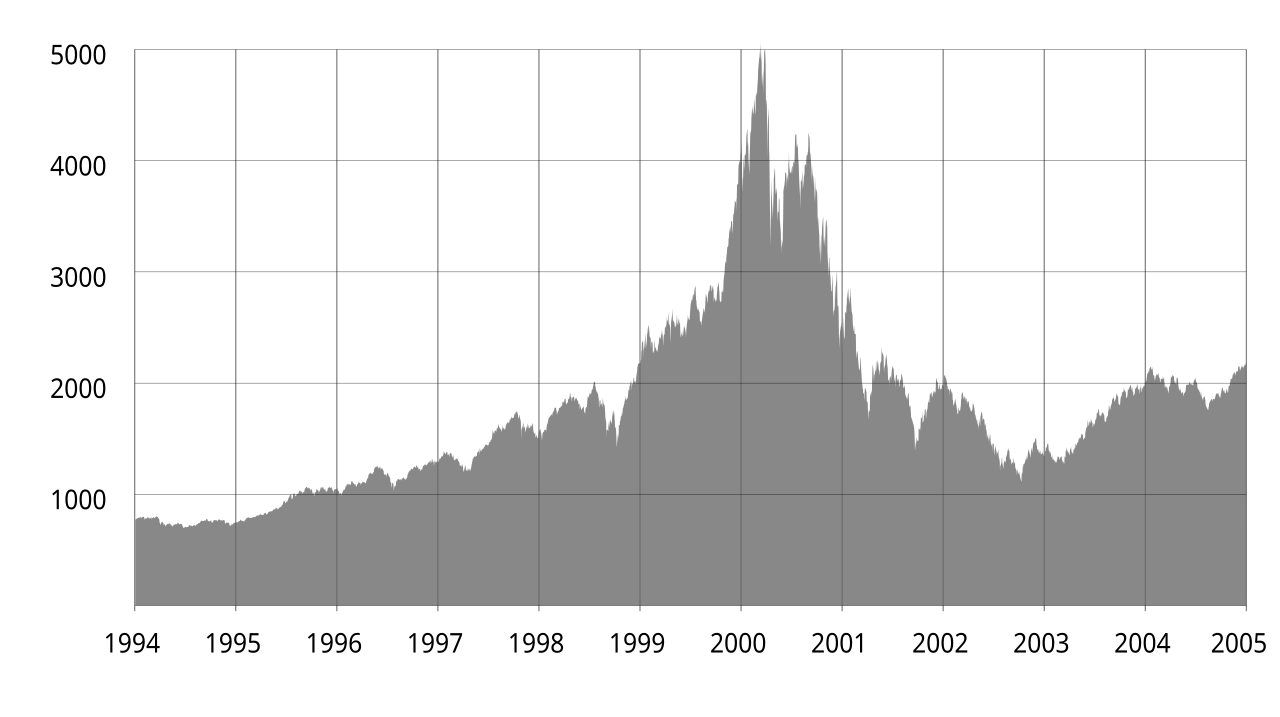

Irrational exuberance is the psychological basis of a speculative bubble. I define a speculative bubble as a situation in which news of price increases spurs investor enthusiasm, which spreads by psychological contagion from person to person, in the process amplifying stories that might justify the price increases, and bringing in a larger and larger class of investors who, despite doubts about the real value of an investment, are drawn to it partly by envy of others’ successes and partly through a gamblers’ excitement.

Robert J. Shiller, Irrational Exuberance

BIBLIOGRAPHY

- Greenspan, Alan. The Challenge of Central Banking in a Democratic Society. Remarks at the Annual Dinner and Francis Boyer Lecture of the American Enterprise Institute for Public Policy Research, Washington, D.C., 5 Dec. 1996. Board of Governors of the Federal Reserve System, 1996.

- Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?

- Harvey, David. The Enigma of Capital: And the Crises of Capitalism. United Kingdom, Oxford University Press, 2010.

- As more surplus capital went into production during the 1980s, particularly in China, heightened competition between producers started to put downward pressure on prices (as seen in the Wal-Mart phenomenon of ever-lower prices for US consumers). Profits began to fall after 1990 or so in spite of an abundance of low-wage labour. Low wages and low profits are a peculiar combination. As a result, more and more money went into speculation on asset values because that was where the profits were to be had. Why invest in low-profit production when you can borrow in Japan at a zero rate of interest and invest in London at 7 per cent while hedging your bets on a possible deleterious shift in the yen–sterling exchange rate? And in any case, it was right around this time that the debt explosion and the new derivatives markets took off, which, along with the infamous dot.com internet bubble, sucked up vast amounts of surplus capital. Who needed to bother with investing in production when all this was going on? This was the moment when the financialisation of capitalism’s crisis tendencies truly began (Harvey 29-30).

- Shiller, Robert J.. Irrational Exuberance: Revised and Expanded Third Edition. United Kingdom, Princeton University Press, 2015.